The Ivey Case

“High-Impact Wealth Management: Jenny and Andrew Confront Mortality”

I was honored to be invited by John Peloza, Finance Lecturer at the Ivey Business School, to speak with his students in London, Ontario.

The case discussed that day — “High-Impact Wealth Management: Jenny and Andrew Confront Mortality” — examines a young professional couple evaluating their financial risks and insurance needs as their careers, assets, and future responsibilities continue to grow.

The students’ task is to analyze Jenny and Andrew’s financial situation and determine an appropriate insurance strategy: how much coverage is required, what type of insurance may be most appropriate (term, permanent, or other structures), what the couple can reasonably afford, and which decisions should be implemented immediately versus deferred to a later stage.

While the case centers on insurance planning, my message to the students was that — from the perspective of sophisticated wealth architecture — the analysis must be approached through a broader strategic lens. The same lens we apply daily when advising families.

For high-net-worth households, these decisions are rarely about purchasing insurance solutions alone. Rather, they involve designing a coordinated financial architecture that integrates protection, tax efficiency, liquidity planning, and long-term family objectives.

In practice, effective wealth management requires stepping back from individual solutions and focusing instead on the process required to engineer durable financial outcomes for families over decades.

Enjoy the case!

Brett P. Nicholson

Founder & President

Senatus Wealth Management Corporation

Disclaimer

The Ivey Case was professionally analyzed by Brett P. Nicholson of Senatus Wealth Management Corporation for educational and illustrative purposes only. The concepts discussed do not constitute financial, legal, or tax advice. Certain facts, figures, and structural elements within the case have been simplified, approximated, or assumed to demonstrate planning concepts.

Readers should consult their own qualified professional advisors before implementing any strategies or concepts referenced herein.

The extent to which this case has been developed exceeds traditional expectations, which is intentional and by design. The reasoning behind this approach will be revealed herein.

Executive Summary

The language in the case was silent on a few critical elements, which have been assumed or approximated herein.

Jenny Li (26) and Andrew Wiggins (28) are a young high-income couple earning a combined $255,000 annually with $551,890 in savings. Jenny is a CPA and Andrew is an entrepreneur.

A recent family death triggered a reassessment of their financial risk exposure and long-term planning.

While their income and savings are strong, their financial structure currently contains several material risks:

Inadequate insurance coverage

Incomplete legal planning

Lack of coordinated corporate and estate structuring

No defined financial outcomes for major life events

Without a coordinated strategy, Jenny and Andrew risk income disruption, estate inefficiencies, and asset misalignment over time.

The recommended approach is a phased financial planning strategy that integrates:

Risk protection

Legal structuring

Corporate planning

Long-term investment growth

For the purposes of this case, some of the following has been assumed and approximated.

Client Overview

Personal Information

Client Age Profession

Jenny Li 26 CPA

Andrew Wiggins 28 Entrepreneur

Financial Profile

Item Amount

Combined income $255,000

Net income $188,135

Annual expenses $90,000

Net free cash flow $98,135

Monthly surplus $8,178 (net)

Savings $551,890

Cash $10,000

Auto loan $8,000 ($30,000 FMV: Toyota Prius)

Catalyst for Planning

The planning discussion was triggered by the death of Jenny’s Aunt Ange.

This event created:

Awareness of mortality risk

Concern about financial preparedness

Motivation to evaluate protection strategies

This type of catalyst is common in financial planning, where life events prompt proactive risk management decisions.

Key Issues

The core issue is lack of integrated planning across risk, legal, and wealth structures.

1. Inadequate Life, Critical Illness and Disability Insurance

Andrew currently has only 1x salary life insurance coverage ($175,000). Neither party has adequate Critical Illness or Disability Insurance.

This would not adequately protect, or preserve their wealth if either Andrew or Jenny passed away.

2. Reliance on Employer Benefits

Jenny and Andrew both rely heavily on group insurance plans, which:

Are tied to employment

May not be portable

Provide limited coverage amounts

3. Lack of Legal Structure

Important legal documents may be missing or outdated:

Wills

Co-habitation agreement

Shareholder agreements

Without these documents, asset distribution and ownership transitions could become complex or disputed.

4. Corporate Structure Uncertainty

Questions remain regarding:

Andrew’s potential corporate structure

The existence of a shareholder agreement within JHOC

Corporate ownership alignment

Jenny’s career movement and access to investment and benefits as she climbs the corporate ladder

This creates uncertainty regarding business succession and asset protection.

Planning Objectives

Before selecting insurance products or coverage amounts, the couple must define their desired financial outcomes at key check points in the future.

Our role as wealth architect is to ensure Andrew and Jenny understand the facts of their situation, outline their options, put them in a position to succeed — providing Andrew and Jenny with clarity.

From here we can begin tosecure adequate insurance coverage on Andrew and Jenny’s lives, and support the insurance solutions with sophisticated planning structures - providing Andrew and Jenny with Control and Confidence

Critical Questions

Our role as strategic advisor depends on understanding the desired future outcomes Andrew and Jenny would prefer to realize. To orient a clear path forward we need to understand the answers to specfic questions surrounding General, Mortality and Life Scenario preferences.

General Questions

When you think about your financial life 10-20 years from now, what would success feel like for you?

Are there any future events where having significant liquidity would be particularly important?

Do you feel your current financial structure is optimized for tax efficiency, or is that something you would like to explore further?

Mortality Outcomes

Key questions include:

What financial outcome should occur if one partner dies?

What financial outcome should occur when both partners eventually pass away?

Life Scenario Outcomes

Additional considerations include, what happens if:

Financial goals are achieved?

Income declines?

Someone gets sick or injured?

The relationship ends?

Holdings are sold?

The answers to these questions define the financial preferences of the couple, then financial architecture and solutions realize those preferences.

Risk Management Tools

Several financial protection tools are available.

Term Life Insurance

Purpose:

Temporary protection

Lower cost, but often most expensive type of coverage for most policy owners

Use cases:

Mortgage protection

Temporary insurance need

Income replacement during working years

Insurability hedge

Permanent Insurance

Includes:

Whole Life

Universal Life

Features:

Feature Description

Coverage duration Lifetime

Cash value Builds over time

Death benefit Can increase over time

Whole Life performance depends on participating fund performance, while Universal Life depends on investment market performance.

Disability Insurance

Purpose: Protect income

Coverage replaces a percentage of income if a client becomes unable to work.

Pricing depends on:

Occupation

Income level

Health history

Approximately 30% of Canadians will become disabled in their lifetime.

Critical Illness Insurance

Provides a lump sum payment if diagnosed with a major illness.

Common covered conditions include:

Cancer

Heart attack

Stroke

Approximately 50% of Canadians will be diagnosed with a critical illness during their lifetime.

Group Insurance

Employer plans may provide:

Life insurance

Disability insurance

Health and dental coverage

Advantages:

Lower cost

Immediate access

Limitations:

Coverage limits

Employment dependency, although some benefits are portable

Mortgage Insurance

Bank mortgage insurance protects the lender, not the client.

Characteristics:

Premiums increase with age

Coverage declines as the mortgage decreases

Private insurance often provides greater flexibility and value.

Legal and Structural Considerations

Key legal elements include:

Estate Planning

Primary and secondary wills

Estate tax planning

Executor authority

Relationship Planning

Co-habitation agreements

Asset division planning

Corporate Governance

Shareholder agreements should address:

Death

Illness

Buy-sell-transfer provisions

Insurance funding mechanics

Asset and Corporate Structuring

A potential ownership structure could include:

Family Trust

Insurance Trust

Investment company(ies)

Operating company(ies)

Benefits include:

Tax planning

Asset protection

Intergenerational planning

Cross-border pipelines

Investment Strategy

Current assets should be evaluated and reorganized for long-term efficiency.

Key strategies include:

Consolidating investments into low-cost diversified ETFs

Reducing portfolio turnover

Lowering management fees

Increasing long-term compounding potential

Jenny and Andrew’s current savings may also serve as seed capital for future corporate investment opportunities, such as private equity, real estate, private loans, and other income producing asset classes that could increase their all-source income.

Net Worth Projection

A comprehensive net worth projection should include:

Net worth today

Net worth in 10 years

Net worth in 20 years

Net worth in 30 years

These projections incorporate:

Investment returns (CAGR)

Taxes (upon sale, transfer and death)

Estate obligations in 10-year intervals

Recommendation

A phased planning strategy is recommended.

Phase 1: Legal Structuring

Immediate priorities include:

Draft primary and secondary Wills (including POAs)

Explore co-habitation agreement

Review and/or establish shareholder agreements

This ensures clear ownership and asset distribution.

Phase 2: Risk Protection

Finally:

Secure life and critical illness insurance coverage

Implement a reimbursement benefit plan structure at Andrew’s company and Jenny’s office

Implement an Income Loss Replacement Plan (ILRP) at both companies

This protects the couple’s income and financial stability while optimizing insurance premiums

Phase 3: Corporate and Investment Planning

Next:

Optimize corporate structure

Implement investment strategy

Develop long-term net worth projections

This stage focuses on wealth growth and tax efficiency.

Implementation Plan

The following implementation should proceed concurrently:

*Insurance applications and underwriting

*Legal document preparation

Corporate (re)structuring

Investment portfolio modernization

Net worth modeling and long-term strategy review

* = Urgent Priority

Risks of Inaction

If no action is taken, Jenny and Andrew face several risks:

Income and net worth loss due to illness, disability, death and taxes

Estate complications

Business succession issues

Higher long-term tax costs

Lack of self-actualization

Early planning reduces these risks and creates financial stability, confidence and peace of mind.

Benefits of Action

Jenny and Andrew are currently in a strong financial position with high income and significant savings for their age. However, their financial structure lacks integration between risk management, legal planning, and wealth strategy.

A coordinated planning approach allows them to:

Protect their income and net worth

Secure long-term financial outcomes

Optimize tax efficiency

Build sustainable, transferable wealth over time.

Outcome: Without and with a Professionally Designed Wealth Architecture

Without Senatus and Professional Wealth Architecture

It would appear that:

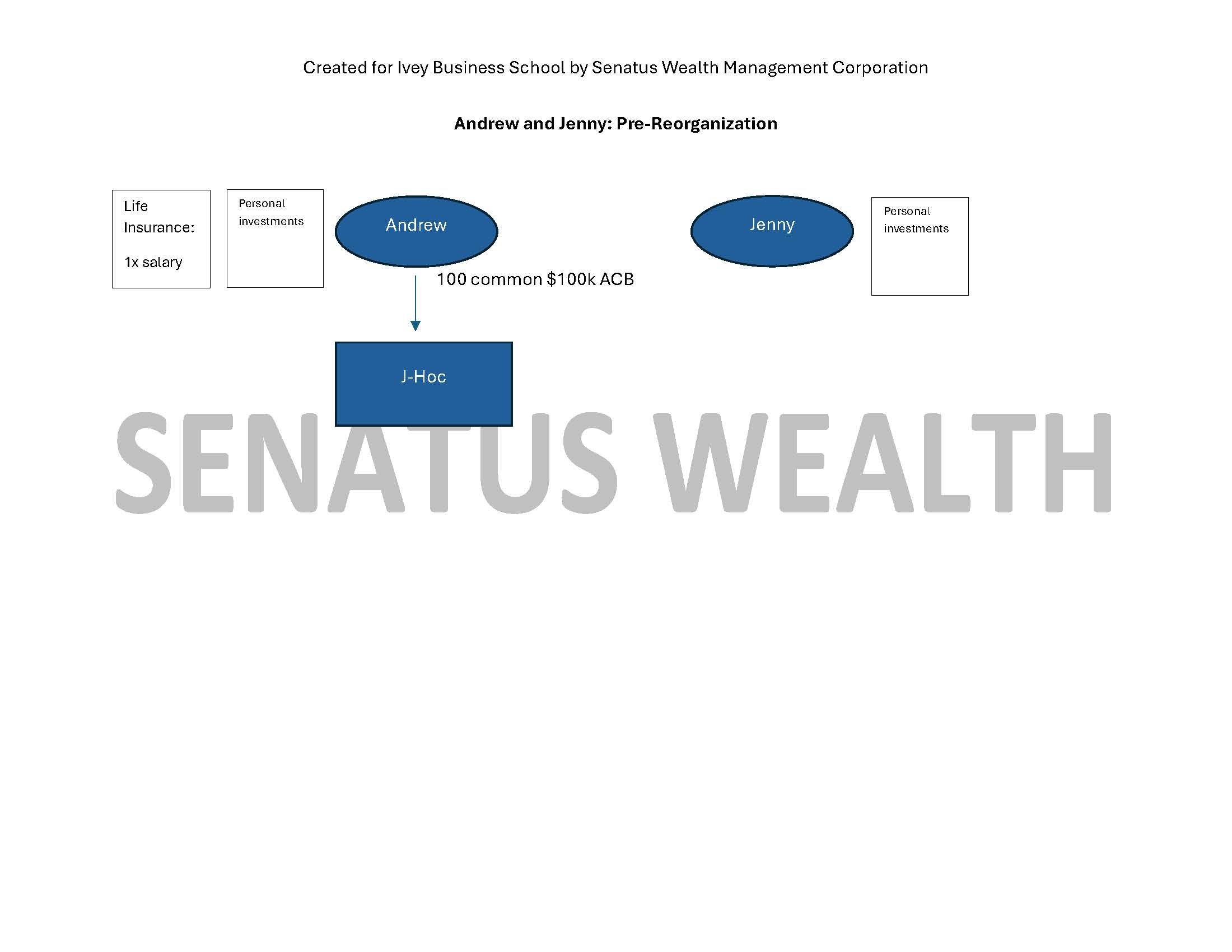

• Andrew owns his shares of J-HOC directly and assumes the role of Vice President, earning a salary within J-HOC

• Jenny is a CPA, salaried employee at APJ & Co. Accounting

• The current structure, reinforced by the tax estimate, indicates single source T1 income, subject to high personal income tax with minimal deduction opportunities

• Inadequate insurance is in force (1x salary on Andrew)

• Income and net worth optimization opportunities are non-existent, if not, limited at best

• Marketable securities portfolios are assumed to be self-managed, hindered by inefficient management

There is no primary home, island property, Florida property, philanthropic plan, accommodation for future children’s tuition, retirement or terminal planning in place

With Senatus and Professional Wealth Architecture

Estate Documents

The estate documents form the legal control layer of the wealth architecture and must align with both the corporate and tax structure.

Testamentary Planning: Wills

Primary and secondary Wills have been established for both Andrew and Jenny. The primary Wills govern personal assets and testamentary wishes, while the secondary Wills address corporate interests and private investments, helping to streamline estate administration and reduce unnecessary probate exposure.

The Wills are drafted with specific consideration of the Income Tax Act (“ITA”). In particular, they accommodate the deemed disposition rules under ITA s.70(5) on death, while including language that allows the executor to implement a spousal rollover election under ITA s.70(6) where appropriate. Alignment between corporate share ownership and testamentary beneficiaries has been incorporated to ensure that succession of corporate interests occurs in an orderly and tax-efficient manner.

The Wills also grant the executors clear authority to implement post-mortem tax planning strategies, including but not limited to loss carryback planning under ITA s.164(6), pipeline planning structures to mitigate double taxation on private company shares, and the declaration of tax-free capital dividends using the Capital Dividend Account (CDA) pursuant to ITA s.83(2). This flexibility allows the estate trustees and professional advisors to implement the most appropriate planning strategy based on the tax environment and asset values at the time of death.

Powers of Attorney

Standard Powers of Attorney for Financial and Medical matters are implemented with specific language to ensure continuity of financial control during incapacity. The language captures corporate voting rights, Banking authority, Insurance policy management, Investment account administration.

Failure to coordinate these documents can paralyze corporate control and tax elections during incapacity.

Personal and Corporate Investments

All personal and corporate investment holdings will be Professionally Managed, invested into a globally diversified portfolio of Exchange Traded Funds. The objectives of the investment plan is to maximize after tax compounding, not simply nominal investment return.

Improving the probability of retaining available investment returns, compounding the assets over time, minimizing investment fees and taxes, and affording Andrew and Jenny daily liquidity will form the basis of the investment management agreement.

The corporate investment portfolio was designed to consider passive income tax rules under ITA s.125 and s.129, and maximize eligible dividend treatment, RDTOH balances and support efficient extraction strategies in the future.

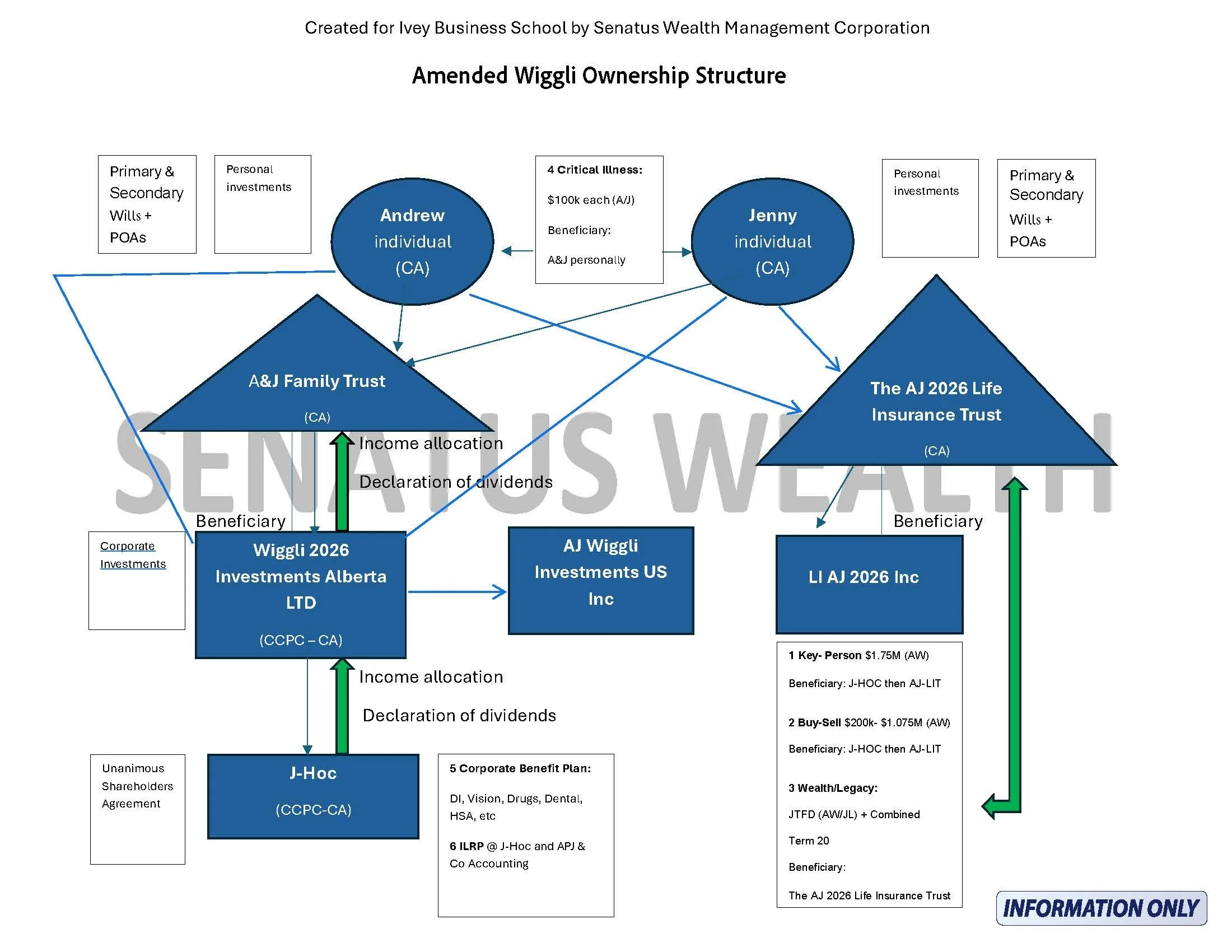

Corporate Structure

A&J Family Trust

A&J Family Trust is implemented to introduce flexibility in wealth accumulation, tax planning, and intergenerational transfer. While considering attribution rules under ITA s.74(4), the trust allows for capital distributions from the holding and operating entities to the trust and then out to Andrew and Jenny tax efficiently. At a future date the trust will be used to shelter capital gains, using trust beneficiaries Lifetime Capital Gains Exemption limits and to offer wealth transfer opportunities under ITA s.110(6). The family was educated on their responsibilities pertaining to the “21-Year Rule”, under ITA. s 104(4) which allows, before the 21st anniversary, assets to be distributed to beneficiaries at tax cost, preserving tax deferral.

The AJ 2026 Life Insurance Trust

The AJ 2026 Life Insurance Trust has been established to separate life insurance ownership from the family’s operating and investment assets while enhancing long-term estate and tax planning efficiency. The trust will own LI AJ 2026 Inc., a dedicated insurance holding company responsible for owning and administering the life insurance policies on Andrew and Jenny.

Premium funding will occur through periodic capital contributions or share subscriptions between the insurance trust and the insurance company. Over time, this structure allows insurance capital to accumulate outside of the operating companies while gradually reducing the Adjusted Cost Base (“ACB”) exposure within the family’s broader estate structure. The result is a gradual shift of value into insurance capital designed to assist with terminal tax mitigation while maintaining flexibility in corporate ownership and control.

Upon the death of an insured, corporate-owned life insurance proceeds will be paid to the insurance company and ultimately flow through the trust structure. The death benefit received by the corporation will generate credits to the Capital Dividend Account (“CDA”), allowing the corporation to elect under ITA s.83(2) to distribute those amounts as tax-free capital dividends to the surviving spouse, family members, or related entities.

The insurance trust structure also integrates with estate freeze planning implemented under ITA s.85 and s.51. Under this framework, founders exchange existing common shares for fixed-value preferred shares, effectively freezing the current value of the business in their estate while allowing all future growth to accrue to newly issued common shares owned by the trust.

Over time, life insurance proceeds can be used to redeem the frozen preferred shares, creating liquidity for the estate while minimizing forced asset sales and preserving business continuity. This approach allows the founding generation to extract value from the corporation in a tax-efficient manner while enabling the next generation to benefit from ongoing business growth.

Wiggli 2026 Investments Alberta

Wiggli 2026 Investments Alberta Inc. has been implemented as a holding company to own Andrew’s shares of J-HOC, providing a corporate structure through which the family can manage and expand future investments. By interposing a holding company between Andrew personally and the operating business, the structure allows for centralized management of investment capital while creating flexibility for future corporate planning initiatives.

Under this arrangement, dividends declared from J-HOC will be paid to Wiggli 2026 Investments, where they may generally be received on a tax-free inter-corporate basis pursuant to ITA s.112. This allows business profits to move from the operating company to the holding company without immediate personal taxation. By retaining these funds corporately rather than distributing them personally, Andrew and Jenny benefit from significantly improved capital accumulation and reinvestment efficiency, allowing surplus capital to compound over long periods of time.

Over time, Wiggli 2026 Investments will also function as the family’s primary investment holding company, capable of owning a diversified range of investment assets. These may include, but are not limited to, real estate, private lending portfolios, marketable securities, and strategic business acquisitions, allowing the family to deploy corporate capital into multiple asset classes while maintaining separation from the operating business.

All Canadian entities within the structure are incorporated in Alberta, Canada, allowing the family to benefit from one of the more favorable corporate tax environments in the country, including competitive small business deduction rates and a business-friendly corporate governance framework, as of the time of this planning presentation.

AJ Wiggli Investments US INC

AJ Wiggli Investments US Inc. has been incorporated in Delaware as a C-Corporation to serve as the operational link between Andrew and Jenny’s Canadian and U.S. activities. The structure supports cross-border business operations while establishing the corporate presence necessary for potential multinational manager immigration pathways, including eligibility to pursue L-1A status and ultimately EB-1C permanent residency classification under U.S. immigration law.

Andrew and Jenny were advised regarding the regulatory and tax considerations associated with owning a U.S. corporation. In particular, discussions included the potential application of Controlled Foreign Corporation (“CFC”) rules, the Canadian treatment of Foreign Accrual Property Income (“FAPI”) under the Income Tax Act, and coordination with the Canada–United States Tax Treaty to mitigate potential double taxation and ensure proper reporting of cross-border corporate income.

The corporation is incorporated in Delaware, a jurisdiction widely used for U.S. corporate structures due to its well-developed corporate law framework, administrative efficiency, and business-friendly governance environment. While Delaware does not impose state corporate income tax on companies that do not operate within the state, federal taxation may still apply depending on the activities and income of the corporation.

The U.S. entity is also intended to act as the petitioning employer with the United States Citizenship and Immigration Services (“USCIS”) for Andrew and Jenny’s immigration pathway. The strategy contemplates securing initial U.S. work authorization, followed by permanent residency and eventual citizenship, subject to regulatory approval and eligibility requirements.

Establishing a compliant U.S. corporate platform enhances the couple’s access to U.S. financial institutions, investment opportunities, and real estate markets, while providing a lawful framework for cross-border business activity and residence planning. This structure aligns with Andrew and Jenny’s long-term objectives relating to U.S. investment exposure, lifestyle flexibility, and family planning across jurisdictions.

Insurance Structure

The insurance portfolio implemented provides risk protection, business continuity and estate liquidity, while complimenting the sophisticated corporate structure.

The following policies were underwritten, secured and placed in-force:

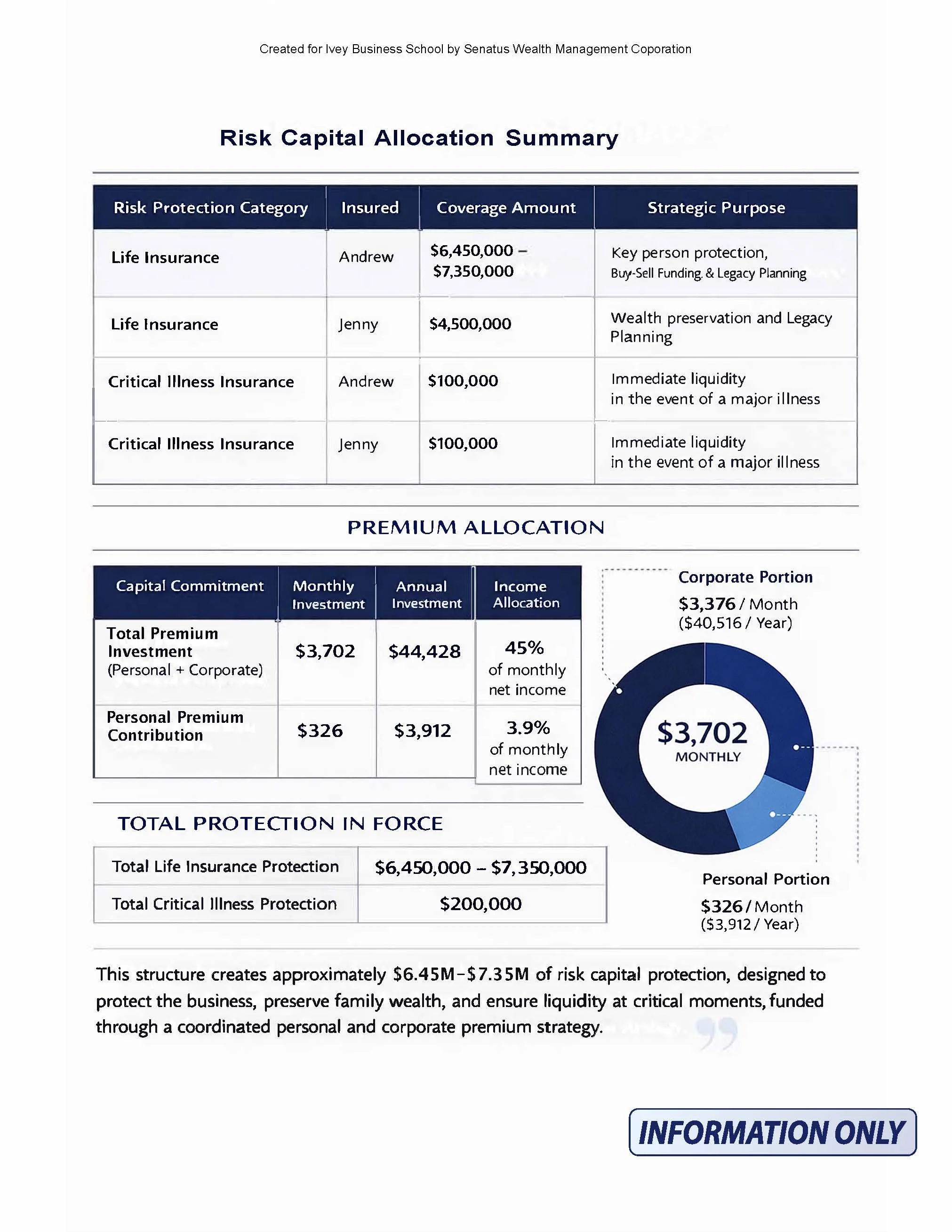

Key Person Life Insurance on Andrew = $1,750,000 Whole Life owned and paid by Wiggli Investments with beneficiary into J-HOC, for an annual premium of $24,575

Buy-Sell Life Insurance + BVP on Andrew = $200,000 - $1,075,00 Whole Life owned and paid by Wiggli Investments with beneficiary into J-HOC, for an annual premium of $713- $2,824

Should the insurance purpose change in the future, beneficiary designations can be updated which does not constitute a taxable event.

Wealth/Legacy/Income replacement coverage on Andrew and Jenny

$1,000,000, Joint First To Die coverage + $3.5M Combined Term 20 coverage — Owned by LI AJ 2026 with a revocable beneficiary designation into The AJ 2026 Life Insurance Trust

$4.5M for an annual premium of $13,117

Critical illness insurance coverage

$100,000 each of Critical Illness Insurance, owned and paid personally by Andrew and Jenny, for a combined annual premium of $3,912

Corporate Benefit Plan

Disability and Corporate Health Benefits within JHOC/APJ & Co/CPA Canada will be implemented under a reimbursement benefit plan structure.

A reimbursement benefit plan, operates on a cost-controlled structure where the employer funds health benefits based on actual claims rather than fixed insurance premiums.

Under this approach, the employer establishes a defined benefits budget and deposits funds into a segregated claims reserve account. When employees incur eligible medical or dental expenses, they typically pay the provider directly and then submit the expense through the Benefits Administrator online portal.

The Benefits Administrator then adjudicates the claim to confirm eligibility under CRA guidelines and the employer’s plan rules. Once approved, the employee is reimbursed directly from the employer’s reserve account, providing a transparent pay-as-you-go benefits structure.

In the Administrative Services Only (“ASO”) model, employers pay only for actual claims incurred while maintaining stop-loss protection. If total claims exceed a predetermined threshold, the excess is submitted to an insurer for reimbursement, protecting the employer from catastrophic claims exposure.

The plan may also include a Health Spending Account (“HSA”), which allocates pre-tax credits to employees that can be used for a broad range of CRA-eligible health expenses. All balances, claims submissions, and reimbursements are managed through the Benefits Administrator portal, with reimbursements typically processed on a weekly, semi-monthly, or monthly basis and accompanied by an Explanation of Benefits (“EOB”) outlining the eligible and reimbursed amounts.

This structure provides employers with predictable budgeting, administrative simplicity, and tax-efficient health benefits, while giving employees flexibility in how they use their health spending allocations.

ILRP

Income Loss Replacement Plan (ILRP) will be implemented at both companies, supporting income protection for Andrew and Jenny should either become disabled.

An ILRP is a corporate disability income strategy that allows an employer to provide employees with disability coverage while achieving tax efficiency and cost control. Under an ILRP, the employer owns and pays the premiums for individual disability policies on employees, and those premiums are generally tax-deductible to the business while not being treated as a taxable benefit to the employee. In the event of disability, the insurer pays income replacement benefits directly to the employee. Although those benefits are taxable, the structure typically allows for higher benefit amounts, often resulting in similar or greater after-tax income protection compared to personally owned policies.

For employers, the ILRP provides a strategic way to protect key employees and stabilize the business during a disability event. It allows companies to define how disabled employees will be supported while avoiding the financial burden of continuing salary payments indefinitely. Because policies are individual contracts, they offer guaranteed renewable coverage, stronger definitions of disability, portability, and the ability to enhance coverage for executives or key personnel beyond typical group Long Term Disability (“LTD”) limits. This makes the ILRP particularly effective for owner-managers and high-earning employees whose income protection needs often exceed standard group benefit plans

Corporate Insurance Summary

Both plans will be funded by each entity, and accommodate other key individuals within each company, creating significant tax advantages compared to personally funded coverage.

Unanimous Shareholders Agreement

The Unanimous Shareholders Agreement (“USA”) governs shareholder rights and corporate governance and is structured to minimize disputes among shareholders while supporting business continuity.

From a tax and legal structuring perspective, several provisions of the Income Tax Act (“ITA”) are relevant to the implementation and operation of such an agreement.

Buy-sell provisions triggered by death, disability, retirement, or incapacity often interact with subsection 70(5), which creates a deemed disposition of capital property at fair market value on death, potentially generating capital gains tax at the shareholder level. Where shares transfer to a surviving spouse, subsection 70(6) may permit a tax-deferred spousal rollover, deferring the recognition of capital gains until the spouse subsequently disposes of the shares.

Where corporate redemption or cross-purchase mechanisms are used to fund buy-sell obligations, section 84(3) may apply to share redemptions by the corporation, resulting in a deemed dividend to the shareholder equal to the amount paid in excess of the paid-up capital of the shares. If life insurance is used to fund the redemption, subsection 89(1) governing the Capital Dividend Account (“CDA”) may allow the corporation to distribute the non-taxable portion of life insurance proceeds as a tax-free capital dividend to shareholders.

If shareholder loans or promissory notes arise in connection with buy-sell funding arrangements, section 15 (shareholder benefits) and section 80.4 (imputed interest benefits) must be considered to ensure that any financial arrangements between the corporation and shareholders are structured appropriately and do not create unintended taxable benefits.

Where insurance premiums are paid corporately to fund buy-sell or key-person obligations, paragraph 18(1)(a) and paragraph 18(1)(b) generally deny deductions for life insurance premiums except in limited circumstances (such as collateral insurance situations under paragraph 20(1)(e.2)). As such, corporate-owned insurance is typically funded with after-tax corporate dollars, while proceeds received by the corporation are generally received tax-free under subsection 148(1).

Finally, valuation provisions and share transfer restrictions within the USA help support the determination of fair market value, which is critical for purposes of capital gains computation under section 38, potential capital gains exemption eligibility under section 110.6, and the proper application of the adjusted cost base rules under section 53.

Together, these statutory provisions inform the tax treatment of the ownership, transfer, and redemption of shares contemplated under the USA and help ensure that buy-sell and succession mechanisms operate efficiently from both a legal and tax perspective.

Reflection

Wealth rarely fails because of poor financial products. It fails because of poor structure and lack of understanding/action pertaining to the desired outcome at critical check points – The improper use of Time, Resources and Communication.

Insurance, investments, corporations, trusts, and legal documents are not solutions on their own—they are simply tools. Their true value only emerges when they are deliberately designed to work together toward a defined outcome.

For Jenny and Andrew, the exercise wasn’t only about determining how much insurance they should buy from a mechanical lens. It was about learning how thoughtful, sophisticated wealth planning transforms uncertainty into structure, risk into resilience, and income into enduring wealth, from a capital engineering perspective.

The proper use of Time, Resources and Communication dramatically improve financial vitality and confidence for Andrew and Jenny.

More broadly, for families who take the time to design their financial architecture properly, the result is not simply protection—it is control, clarity, and the ability to shape outcomes for generations.

That is the essence of high-impact wealth management.

Take Action

If the ideas outlined in this article resonate with your experience, the next step is a conversation.

Many of the families and business owners we work with arrive at similar questions: how to structure their wealth, reduce friction across entities and jurisdictions, and design outcomes that endure across generations.

If you would like to discuss your situation privately, you can reach me directly at brett@senatuswealth.com.

If you believe someone in your network would benefit from the perspectives shared in this article or others, please forward the article to them.

For those seeking a more comprehensive review, private advisory consultations can be scheduled here.

To learn more about how we organize, structure, and oversee complex wealth for business owners and high net worth families, visit Senatus Wealth Private Advisory, and reach out to schedule a productive consultation.