Enjoyed by Generations, for Generations: Preserving Emotionally Significant Assets Through Tax, Legal, and Liquidity Design

Engineering clarity, control, and confidence for Canadian families, including those with cross-border planning needs.

Practitioners may wish to keep this article in mind when the next high-net-worth succession file arises. We would welcome the opportunity to collaborate in a manner that benefits the client, supports your practice, and elevates the quality of the planning overall.

About This Article

Some assets matter to a family in ways fair market value cannot explain.

A cottage, company, collection, or legacy property may be measured in dollars, but its true significance often lies in memory, identity, and continuity. The technical issue is not whether the family loves the asset. It is whether the ownership, governance, liquidity, and tax architecture around it have been designed well enough to preserve it when pressure arrives.

This article offers a sophisticated Canadian framework for minimizing avoidable wealth erosion and improving the probability that important assets remain part of a durable family legacy.

Certain U.S. planning considerations are addressed in this article, but they are not its principal focus.

Executive Summary

Without serious planning, important family assets are exposed to tax, legal, and liquidity pressure at exactly the wrong time. In Canada, subsection 70(5) can create tax at death without a sale. Subsection 70(6) may defer that outcome, but often only defers the strain. Trusts may improve stewardship, but section 104 and subsection 104(4) impose their own tax discipline.

Where private-company wealth is involved, outcomes may turn on the careful interaction of sections 15, 20(1)(c), 85, 86, 84, 87, 88(1), 84.1, 128.1, and 164(6). These rules matter because sophisticated planning is rarely about one provision in isolation. It is about sequencing, characterization, and preserving optionality before it is lost.

Properly structured insurance is not merely protection. It is liquidity architecture. It can fund tax, support equalization, preserve control, and help keep significant assets inside the family system.

The point is not simply efficiency. It is continuity.

The Problem Is Rarely Affection. It Is Architecture.

Most families already know what matters.

They know the cottage is more than real estate. They know the family business is more than enterprise value. They know the art, the cars, the properties, and the family places carry a significance that cannot be recreated once lost and cannot be captured by fair market value alone.

What is often missing is not affection, but architecture.

Families may be deeply committed to preserving what matters, but intention alone has no legal force. The law does not preserve a cottage because it has hosted four generations. The Income Tax Act does not moderate a deemed disposition because a business was built through sacrifice. Sentiment does not create liquidity. Affection does not resolve equalization. Memory, however important, is not a planning framework.

Without careful design, wealth that appears formidable can prove structurally delicate. A family may have substantial net worth and still be forced into bad decisions when death, incapacity, marital breakdown, tax, cross-border exposure, governance weakness, or disputes over fairness put pressure on the file.

That is how continuity is lost.

Not through indifference, but through administrative failure.

A Familiar High-Net-Worth File

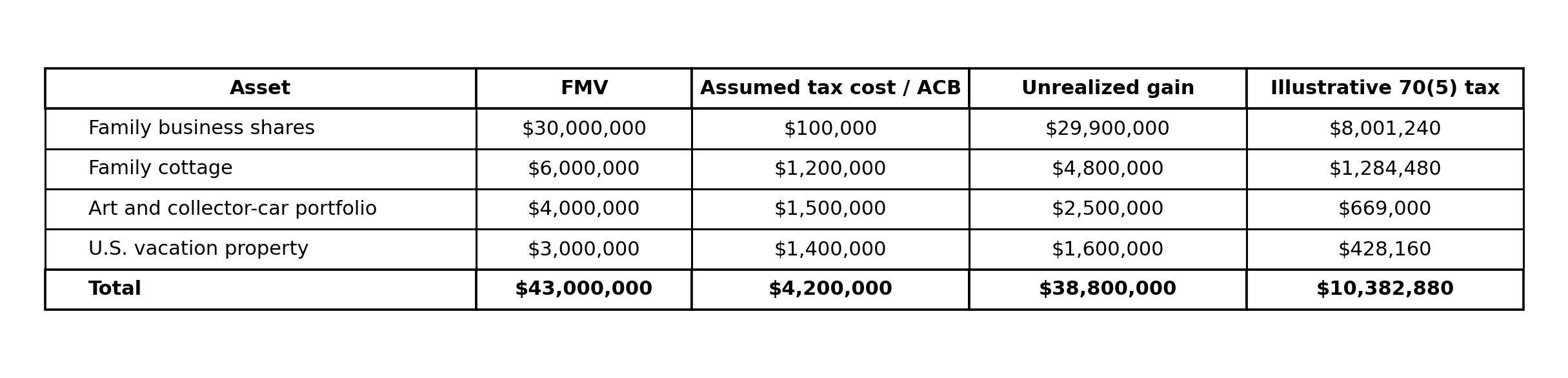

Consider a Canadian family with a substantial but highly concentrated balance sheet.

The parents hold a family business worth approximately $30 million, a cottage worth $6 million, a meaningful art and collector-car portfolio worth $4 million, and a U.S. vacation property worth $3 million. Much of the family's wealth is therefore real, but illiquid. It exists in assets that matter deeply but cannot easily satisfy tax and equalization demands without being sold.

There are three adult children.

One is active in the business and expected to continue building it. One is deeply attached to the cottage and sees it as part of the family's identity. One is financially sophisticated, U.S.-resident, and less interested in preserving illiquid family assets than in retaining financial flexibility.

This is where simplistic ideas about equality begin to fail.

If one parent dies holding appreciated capital property and no meaningful planning has been done, subsection 70(5) will often impose a deemed disposition immediately before death at fair market value. If a qualifying subsection 70(6) rollover is available, the tax may be deferred on the first death, but the underlying gain has not disappeared. It has merely been deferred.

Illustrative Subsection 70(5) Exposure in the Absence of Planning

Illustrative assumptions: The figures below assume the deceased was resident in Ontario, already exposed to top marginal personal rates, and that the 50% capital gains inclusion rate continues to apply. The calculation uses an illustrative Ontario top marginal tax rate on capital gains of 26.76%, based on a combined top ordinary income rate of 53.53%, and excludes Ontario Health Premium, probate / estate administration tax, U.S. estate-tax or U.S. income-tax consequences, capital gains exemption relief, recapture, rights-or-things exposure, and AMT. The tax costs below are assumed only for illustration.

Exclusive intellectual property of Senatus Wealth Management Corporation

Under these assumptions, the family's subsection 70(5) exposure alone is approximately $10.38 million on the first death if no rollover or other relieving rule applies. That figure does not describe a sale. It describes a tax liability triggered by deemed disposition. For many families, that is the moment when a cherished asset stops being a legacy question and becomes a forced-liquidity problem.

At that point, the family is not making a stewardship decision. It is making a financing decision under duress.

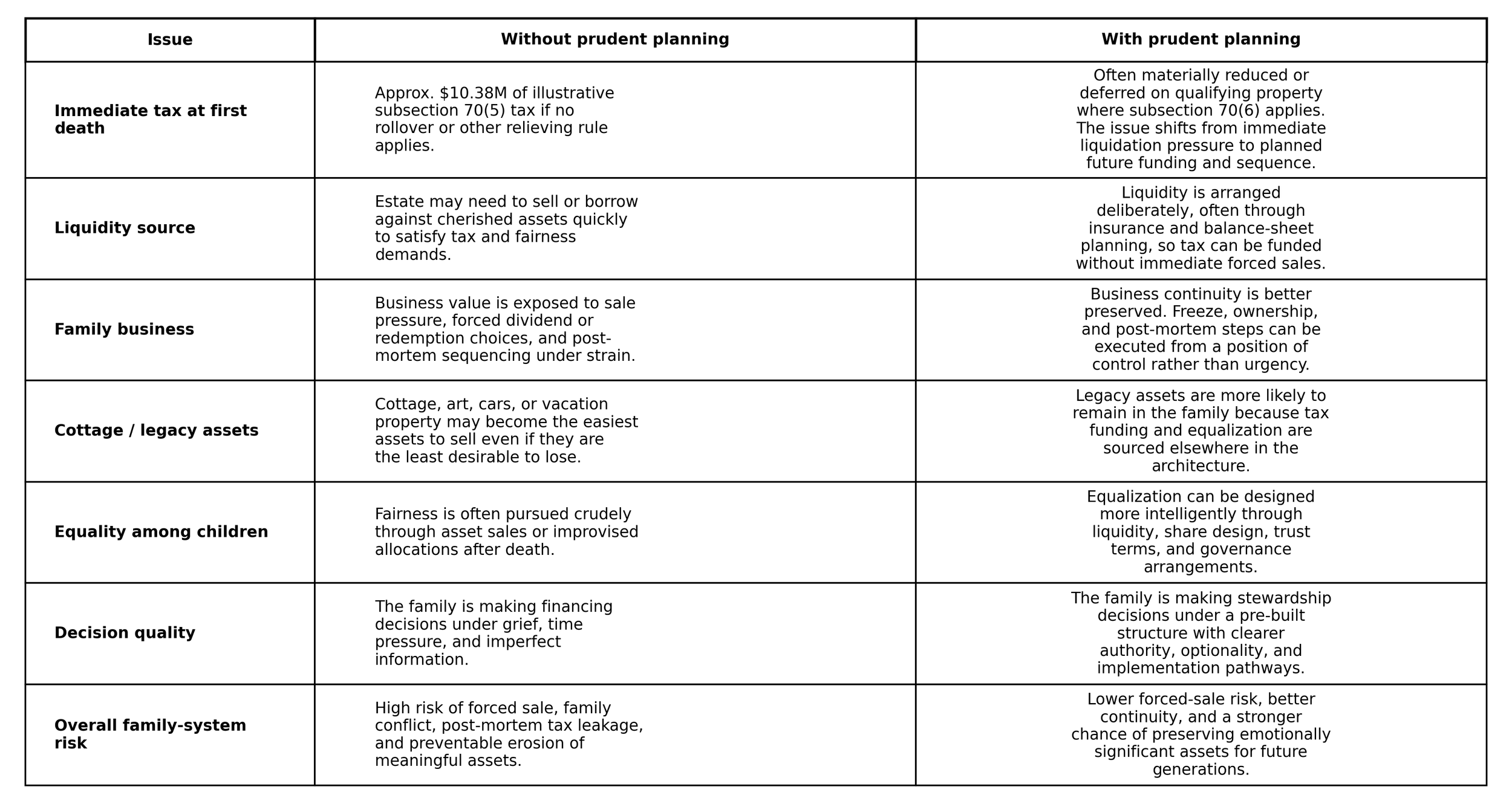

Illustrative Comparison: Without Planning vs. With Prudent Planning

The comparison below is not a formal tax opinion. It is a planning illustration showing how disciplined tax, legal, liquidity, and succession design changes the family's economic and practical position. The 'with planning' column assumes the family has completed integrated work that may include a qualifying subsection 70(6) rollover on first death, coordinated will and trust drafting, governance design, estate-freeze architecture where appropriate, and insurance-based liquidity to fund eventual tax and equalization rather than forcing asset sales.

Exclusive intellectual property of Senatus Wealth Management Corporation

Illustrative calculation note: The 70(5) tax estimate above is a planning illustration only. Actual terminal tax will depend on final valuations, adjusted cost base, available losses, deductions, principal-residence status, LCGE availability, foreign-tax interactions, AMT, provincial residence, and the ultimate implementation sequence.

The Real Role of Planning

Sophisticated planning does not usually make tax disappear. It does something more useful. It changes the character of the problem.

A tax issue that would otherwise force liquidation becomes a problem of sequencing, control, and funding. A family that might have sold the cottage can now retain it. A business that might have been partially dismantled to fund fairness among heirs can continue intact. Assets that are emotionally indivisible can remain in place because liquidity was arranged elsewhere in the system.

A qualifying subsection 70(6) rollover can defer immediate realization on the first death where its statutory requirements are met. That can be profoundly valuable, but it is not magic. It is a deferral rule. It buys time and preserves optionality. It does not eliminate the need for a durable solution.

Trust planning can improve governance, continuity, and stewardship, but only where it is approached with rigor. Section 104 is not an elimination citation. It is part of the operative trust-tax framework, and subsection 104(4) means that a trust can itself become the site of a future deemed disposition if the planning has merely postponed the family's problem rather than solved it.

Cross-border families face even greater complexity. Once a beneficiary, trustee, executor, or controlling family member becomes U.S.-connected, what once appeared to be a domestic Canadian estate plan can become materially incomplete. Residence, situs, reporting, ownership, and departure or immigration analysis begins to matter differently. In those files, Canadian tax analysis may also intersect with subsection 128.1 and treaty-sensitive structuring questions. As you know, our compliance friends south of the border can be quite intrusive.

This is why the most valuable work in these matters is rarely a single tactic. It is the disciplined orchestration of many.

The Valuable Tax and Legal Work

The most sophisticated files generate meaningful tax and legal work because they require genuine integration.

There is legal work in redesigning ownership, revising wills, structuring trusts properly, establishing governance mechanisms around a cottage or vacation property, aligning share rights with the family's preferred intentions rather than a generic cap table inherited from an earlier era, and drafting occupancy rules, cost-sharing terms, dispute-resolution frameworks, trustee powers, and succession mechanics intended to function not merely on paper, but within the family.

There is tax work in modeling subsection 70(5) exposure, confirming whether subsection 70(6) is available and strategically useful, analyzing section 104 and subsection 104(4), addressing shareholder-benefit exposure under section 15, validating paragraph 20(1)(c) deductibility, and preserving post-mortem optionality where the facts support it.

In a private-company death file, the real work usually begins after subsection 70(5), not before it. The file may require integrated analysis of subsections 84(2) and 84(3), section 87, subsection 88(1) including paragraph 88(1)(d), subsection 164(6) (thanks for the extended time, Mark), and section 84.1 as a collateral constraint on adjacent non-arm’s-length steps. Subsection 84(3) is the redemption, acquisition, or cancellation rule and generally deems a dividend to the extent proceeds exceed paid-up capital. Subsection 84(2) is broader and may recharacterize distributions or appropriations of corporate funds or property made on a winding-up, discontinuance, or reorganization of the business, including in post-mortem extraction contexts. Section 87 matters only where the structure actually involves a qualifying amalgamation of taxable Canadian corporations. Paragraph 88(1)(d) is not a planning shortcut; it is a conditional bump embedded in the subsection 88(1) wind-up framework and is available only if ownership and sequencing have been preserved with care. Subsection 164(6) may offer substantial relief, but only if the election is properly made, and every statutory condition is met. Meanwhile, section 84.1 can quietly contaminate nearby succession-driven share sale transactions, even where the commercial narrative is entirely non-abusive. In a serious death file, these provisions do not operate in isolation. They interact, and the result is determined less by intention than by structure, control, and sequence.

None of this work is ancillary. It is the difference between continuity and preventable erosion.

Insurance as Liquidity Infrastructure

Insurance is often spoken about too narrowly in wealthy families, as though its relevance begins and ends with a death benefit. At a higher level of planning, insurance should be understood as liquidity infrastructure.

It can fund tax without forcing the sale of the cottage. It can supply equalization capital to a child who will not receive the business. It can allow the family to preserve an art collection intact rather than fragmenting it to create fairness. It can support post-mortem implementation. It can stabilize the estate's balance sheet precisely when other assets are illiquid, indivisible, or strategically too important to dispose of.

Where a corporation has the relevant interest in a life insurance policy and receives the death benefit, the amount added to the corporation's capital dividend account is generally the death benefit net of the policy's adjusted cost basis immediately before death. That can create a materially more efficient extraction path, but only if legal ownership, beneficiary designations, and post-mortem implementation are coherent. Section 148 remains relevant wherever a disposition or deemed disposition of an interest in a life insurance policy is in view.

That is why insurance, in sophisticated files, is not an isolated product discussion. It is part of the family's capital architecture.

An insurance trust may also have a role where the family wants tighter governance and stewardship over proceeds. The trust must be real, properly documented, and administered consistently with its legal and tax design. The point is not opacity. It is precision.

Freezes, Section 86, and the Allocation of Future Growth

Estate freezes remain one of the most important structural tools in these files, but even here the commentary should remain precise.

A common-for-preferred exchange may often be implemented under section 86, but sophisticated practitioners know that many freezes are broader than section 86 alone and may also engage section 85, rights design, valuation work, and corporate-law amendments. Section 86 must therefore be read in transactional context rather than in isolation.

The value of an estate freeze is not merely that it locks in value. Its deeper value is that it separates accrued legacy value from future entrepreneurial growth. Over time, that separation becomes increasingly important. The senior generation’s preferred shares typically reflect the crystallized value of the business at the time of the freeze, while new common shares are positioned to capture future growth in the hands of those intended to benefit from it. Once that architecture is in place, family equalization can be approached with greater precision and far better judgment.

Practitioners sometimes supplement this with tracking-share design. Tracking shares are not a defined statutory term. Their usefulness lies in corporate design, valuation discipline, and enforceable implementation. Used properly, they can help differentiate economic entitlements so that insurance-related value does not wash indiscriminately across the entire capital structure regardless of the family's actual succession objectives. Used poorly, they simply introduce ambiguity into an already sensitive file.

What Happens Without Sophisticated Wealth Architecture Engineering

In the absence of this level of planning, families often create outcomes that are superficially equal and substantively destructive.

One child receives a business but also the burden of continuing it. One receives a beloved but expensive property. One receives liquid capital and appears, in practical terms, to have done best. The estate leaks tax inefficiently. Family members argue not only about value, but about labor, identity, sacrifice, entitlement, and memory.

At that stage, the issue is no longer merely technical. It is relational.

The family did not fail because it lacked wealth. It failed because it did not convert wealth into durable structure before complexity arrived.

Too many Canadian families do not recognize the problem until pressure is already applied. By then, the choices are narrower, the tax work is less elegant, the legal work is more reactive, and the family is often negotiating under strain instead of designing from strength.

That is the real cost of delay. And we can help you engineer away from this eventuality.

Key Takeaway — Continuity is not inherited. It is engineered.

A family cottage, a business, a collection, or a vacation property does not remain in the family because it is loved.

It remains because the family and its advisors were disciplined enough to build a prudent wealth architecture around it.

The most valuable tax and legal work in these files is not technical cleverness for its own sake. It is the preservation of continuity. It is the protection of optionality. It is the disciplined coordination of ownership, governance, liquidity, succession, and post-mortem tax mechanics so that the family's most meaningful assets are not surrendered to avoidable tax, structural neglect, or poorly designed fairness.

It takes a disciplined architect to align the family, the advisors, and the preferred outcome. That is where I come in.

The ideal result is clear: important assets remain where they belong, enjoyed by generations, for generations.

Next Step: Take Action

If the ideas outlined in this article resonate with your experience, the next step is a conversation. Many of the families and business owners we work with reach similar checkpoints and begin considering how to:

· Structure their wealth.

· Reduce friction across entities and jurisdictions, and

· Design outcomes that endure across generations.

If you would like to discuss your situation privately, you can reach me directly at brett@senatuswealth.com, and if you believe someone in your network would benefit from the perspectives shared in this article or others, please forward the article to them.

For those seeking a more comprehensive review, Private Advisory Consultations can be scheduled here.

To learn more about how we organize, structure, and oversee complex wealth for business owners and high net worth families, visit Senatus Wealth Private Advisory, and reach out to schedule a productive consultation.

Additional, public resources are accessible on our website through Perspectives, with Advanced Perspectivesand Professional Perspectives available for exclusive membership.